10 reasons to convert Traditional IRA/401k to Roth IRA/401k.

…or for the younger crowd - why contribute to your Roth IRA/401k.

1. We are in lower tax brackets under the 2017 tax code revisions.

Our current tax brackets are expanded in size and lower in rate then the brackets we were in during prior decades. The 2017 TCJA personal tax brackets (and other changes) are set to sunset in 2025 back to former status. Many also believe that the new administration will likely increase personal income tax rates prior to this sunset date.

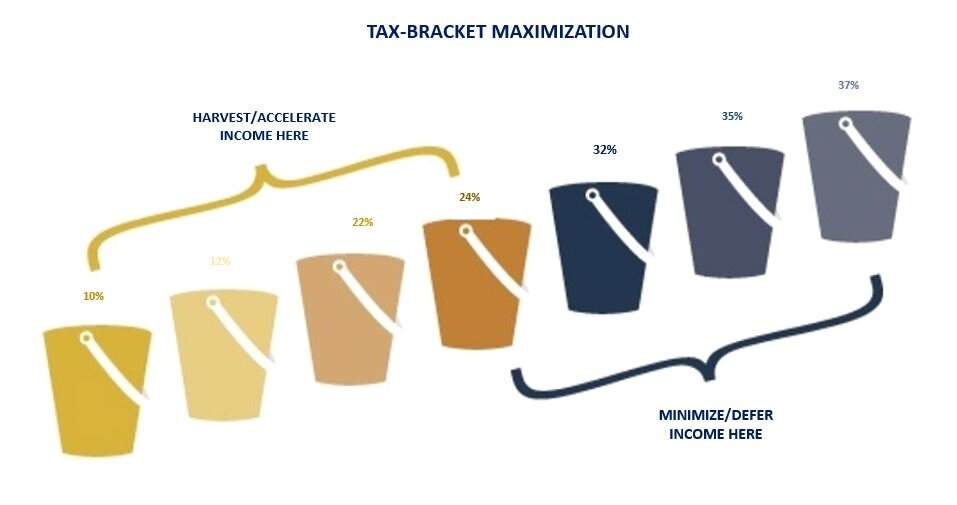

The new (current) tax brackets are 10%, 12%, 22%, 24%, 32%, 35%, 37%.

The old (and likely future?) brackets are 10%, 15%, 25%, 28%, 33%, 35%, 39.6%

Most middle class couples looking at converting will find themselves in the 3rd tax bracket. For a married couple - this means your taxable income is between 81k-172k (roughly). Remember, your taxable income is your gross income, less adjustments, then subtract your itemized/standard deductions. (You may make $150,000 but only have taxable income of $105,000) If your taxable income is only $105,000, you could convert up to the top of the current bracket (22% up to 172k) and not be in a higher tax bracket. You could even convert higher into the 24% (which goes up to $330,000 of taxable income) and still be paying “less” than what the old (and likely future) tax brackets would have you pay at the 3rd bracket rate of 25%!!!

2. You are married but someday your surviving spouse will be in a higher single bracket.

The first few tax brackets are doubled for those married (filing jointly) compared to single filers. While we’d like to envision a peaceful passing at the same time as our spouse, many find themselves widowed for 1-2 decades after their spouse passes. At the death of the first spouse, expenses reduce - but typically to about 60-70% of the former joint expenses. In addition, social security reduces (to the larger of the two benefits). While the widowed spouse is “spending less” - between the reduction in social security benefits and the (likely) INCREASE in taxes (due to compressed single filer brackets), they ironically find themselves having to take larger distributions from their retirement accounts. If converted when married, the spouse can favorably access the Roth IRA without paying more in tax.

3. You can keep your tax bill lower on your future social security benefits.

This is known as the “tax torpedo” when your taxable income ends up dragging your social security benefits into a taxable status. Your social security retirement benefit may (or may not) be included in your taxable income depending on your other taxable income. Basically anywhere from 0% to 85% of your benefit might be subject to federal income tax depending on your “provisional income” (another IRS complexity - but mainly driven by your taxable income). Here is the deal - for some this won’t matter because their taxable income is going to be too high regardless (they have pensions, real estate income, or other taxable income that puts them above the thresholds). For others, they don’t have enough assets/income to trigger inclusion. For many (actually most- think middle class), their taxable IRA/401k distributions will put them in a situation where they unintentionally pull their social security benefits from a non-taxable status into a taxable status. This could have potentially have been avoided (or minimized) by Roth conversions (or contributions to Roth) prior to claiming Social Security. (ties in to point #6)

4. You don’t want to be told what to do with the money in retirement.

Lets face it - if you have a traditional account, every decision you make involves you AND the government. This is a painful conversation and a constant reminder that you don’t have total control over your money. If you want a big lump sum (for a new vehicle, cabin, large vacation, etc…) you might feel “bullied” into taking a loan or paying a big tax bill as you find yourself flying up a tax bracket (or two) with this large distribution. When you have funds in your Roth IRA, you get to control what tax bracket you top out in and how you pay for things! Want to pay lump sum for a car? Withdraw $50,000. Don’t feel like dealing with a bank loan for a new condo? Take $200,000 from your Roth. (and don’t worry about the taxes!!)

Your traditional accounts will have required minimum distributions (RMDs) starting at age 72 (formerly 70.5). You CAN’T convert your RMDs to Roth! If you have a big balance in your traditional accounts, you’ll be forced into large distributions that won’t give you as much flexibility in your tax strategies (point #3 and #6).

5. You want your heirs to have access without severe taxation.

It was already bad… now its terrible! There are a few exceptions but your children will be expected to distribute your IRA within 10 years of inheriting (Roth or Traditional). The “old rules” allowed “stretching” the distributions over their lifetime (in a modified Required Minimum Distribution), but now you have 10 SHORT YEARS to fully distribute the inherited account. If this is a large traditional account - this could mean SEVERE taxation in higher tax brackets added on to your working income. Very likely, the older parent(s) who died, were in a lower tax bracket and would be better off converting and paying the tax for their adult children. This scenario could be even worse - if you are in your 50s with a kid in college and inherited a traditional IRA from your 80yo parent, your taxable distributions might disqualify your student (child) from financial aid or the tax credits for college.

6. You want to have “tax flexibility” in your annual retirement distributions and spending.

This is what we call “playing the bracket game…” You can always control how much tax you pay, what bracket you stay in, and your adjusted gross income (AGI) by having Roth and traditional funds. A common strategy would be to make sure you stay in the 1st/2nd tax brackets (currently 10/12%) without going up to the 3rd bracket (22%). If you need funds for expenses over the second bracket, you take distributions from your Roth IRA! This allows you to have constant control over how (little) you pay taxes in retirement. You can make sure you aren’t dragging your social security benefit into an excessive taxable state (point #3) while still maximizing your standard deduction with traditional distributions.

7. You could have access to the principal before 59.5 without a penalty tax.

All retirement plans have a penalty tax before 59.5 right? Well, yes… but for Roth IRAs this is ONLY on the earnings! Roth IRAs allow you to access your CONTRIBUTIONS FIRST without tax or penalty (tax)! While not meant to replace a liquid savings account, this does allow for partial liquidity, emergency protection, and flexible distributions if needed before 59.5! Buying into a business? Sending a kid to college? Paying off high interest debt? Down payment on a home/2nd-home? If you’ve been contributing to your Roth IRA for years, you’d have a hefty balance of accumulated contributions that would be accessible! Make sure you leave the profit (earnings) alone to 59.5 (as there’d be income tax + penalty tax). There are also special rules on accessing Roth conversions before 59.5 - but too much detail for this section.

8. You have excess cash on hand that could be used to pay the conversion tax.

If some of these other points make sense and you are wondering what you could do with extra cash on hand - think of “investing it” by using it to pay the tax on a conversion from traditional to Roth. While you could withhold tax from your converted amount (convert $20,000 and withhold $5,000 to cover taxes, leaving you with $15,000 in the Roth), it’d be better if you have extra cash available to pay for the conversion directly (so you convert $20,000, pay the $5,000 tax bill from an outside account, leaving $20,000 in your Roth to grow tax-free!).

Also, be careful if converting before 59.5. If you didn’t pay the tax from non-retirement funds (ie. your bank account), the tax withheld inside the conversion will count as an early distribution and you’ll be penalized for it. If you are converting before 59.5, it is ALWAYS recommended to cover your tax liability separately. If you are over 59.5, it is still recommended to pay the tax with outside funds, but if you do pay internally at least you aren’t penalized for it.

9. You are moving from a state with no income tax to a state with an income tax.

Many times you might be moving to a state with high tax to low/no income tax (think retiree states like Florida or Texas). But sometimes you might be moving from Texas to Arizona or Florida to California. If you convert before moving to a “high tax state,” you can avoid paying a higher future state income tax! Do be careful on taxation the year you move states as you typically file tax returns in each state - likely better off to do the full year prior.

10. Keep more aggressive investments in your Roth and income producing/conservative investments in your Traditional.

I refer to this as “asset location” (not to be confused with “asset allocation”). Why not place your more aggressive funds/securities in the tax-free-forever account with no RMDs!! Likely this lines up with your distribution strategy anyways - leaving your Roth for longer term needs (surviving spouse, inheritance, etc…) which naturally lends itself to a more aggressive stance. You typically will be using your traditional accounts for ongoing/systematic distributions to cover base/fixed expenses - so keep your taxable accounts heavier with fixed income.

As an example of this - someone might be a “moderately aggressive” investor with an overall asset allocation of 70% equities and 30% bonds. Typically they’d have all their accounts with similar investments to match this asset allocation. Why not dial back your traditional accounts to 50/50, and dial up the Roth accounts to 90/10 (as a simplified example)? Overall, you’ll still be a 70/30 “moderately aggressive” investor but you are now allowing your tax-free-no-RMD account to have more growth potential and making your distributions/taxable account (traditional IRA/401k) more balanced/conservative!

11. Bonus reason - when the market drops/dips.

Lets call this “making lemonade out of lemons…” When the market drops 10-30% you get to convert the same # of shares at a discount, pay the tax on a lower amount, and then the “rebound growth” along with all future growth is tax free! There are only a few decent things to do when the market goes down: rebalance your funds, tax-loss harvest, and convert traditional accounts to Roth! This strategy is best if you already were planning to convert systematic amounts (yearly in the 4th quarter, for example) - if the market dips in 2nd quarter why not take care of your planned Roth conversions right then and there!

If you had done this during the 2020 COVID market downturn, you’d have likely converted assets at a 30% discount! Keep in mind, you can’t “time the market” to always hit the exact drop (or know how long it will take to rebound…) - but the principal is converting at some sort of discount is always better than the former higher price!

Putting this all together - any one or two of these reasons might be enough to suggest a conversion. If you have 3-5+, you should strongly consider! Here is is an example scenario that appears prime for a Roth conversion: Pre-retiree or recent retiree younger than 72 (point #4), married (point #2), has funds in the bank (point #8), in the 2nd/3rd tax bracket (point #1), potentially hasn’t started taking social security yet (point #3), has saved enough they will likely leave behind a substantial inheritance to their kids (point #5).

Reasons not to convert, other considerations, and a disclosure:

First of all, this isn’t meant to be taken as specific advice. Consult your financial professional and/or tax advisor to understand what makes sense for you.

You likely don’t want to convert too big a chunk all at once. Many times, a “conversion strategy” should be formed and you should convert strategic amounts over a number of years to maximize your tax savings.

There are adverse consequences to conversions - you might have disqualified yourself from a stimulus check (for example, if you converted in 2020), made your self ineligible for other tax credits (be careful converting if you are filling out FAFSA or claiming education credits), or have other needs-based assistance that is based on your adjusted gross income.

There is such a thing as converting TOO much. You have a big standard deduction in retirement and could take traditional IRA/401k distributions up to the standard deduction and not pay a dime of tax (depending on other factors). You also could use your traditional IRA after age 70.5 to make qualified charitable distributions to a charity/non-profit which is superior to trying to itemize a deduction or using Roth funds to donate. Converting the RIGHT AMOUNT is important!